Blog / June 13, 2026

At the Top of the Market, Premiumization Is Still Winning

In 2025, U.S. spirits revenue fell in every price tier but the most expensive. The top shelf grew; everything below it traded down — one bottle at a time.

By Zillah Bahar, Founder, COLAClear · June 13, 2026

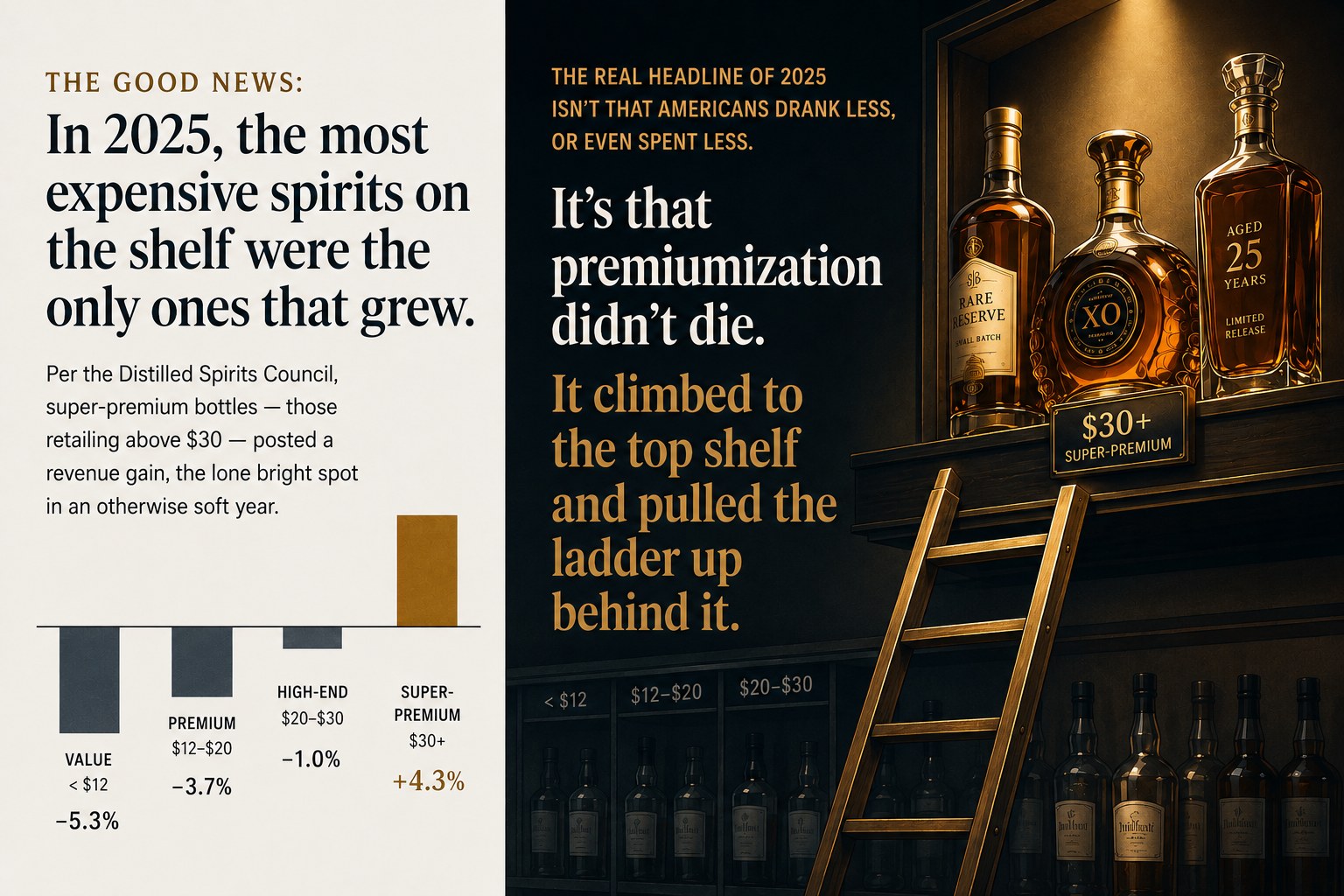

Start with the good news: in 2025, the most expensive spirits on the shelf were the only ones that grew. Per the Distilled Spirits Council, super-premium bottles — those retailing above $30 — posted a 4.3% gain in U.S. supplier revenue, the lone bright spot in an otherwise soft year. They did it on fewer bottles, too: super-premium volume actually slipped, which means the drinkers who stayed paid roughly 8% more per bottle than the year before. At the very top of the market, premiumization isn’t just intact — consumers are absorbing price increases without blinking.

Then comes the staircase. Step down one price tier at a time and the picture darkens. Revenue of high-end premium ($20–$30) dipped 1.0%. Premium ($12–$20) fell 3.7%. Value (under $12) dropped 5.3%. The cheaper the bottle, the worse the year.

That single pattern is the story of 2025. Total spirits revenue fell 2.2% to $36.4 billion, but the softness isn’t spread evenly — it’s concentrated at the bottom and the middle, exactly where the squeezed consumer shops.

Why it’s happening

The cause isn’t a mystery: Consumer sentiment fell to historic lows in 2025, while stubborn inflation — especially in the non-negotiables like housing, healthcare, and insurance — kept eating into discretionary income. Younger adults, newer to the workforce and with less spending power, felt it most.

That’s a textbook K-shaped split, and it sorts drinkers by income. The affluent super-premium buyer is insulated; a $45 añejo or a single barrel is a rounding error in their budget, so they keep buying — and keep trading up. The everyday and aspirational drinker is exposed; when the mortgage and the insurance bill climb, the $15 bottle is the first place they economize.

And here’s the part that matters most: they aren’t leaving their favorite categories — they’re trading down within them. Tequila is the clearest tell. Its revenue fell 4.1% while volume stayed essentially flat (−0.3%). People still wanted tequila; they just reached for a cheaper expression of it. The same downshift runs through vodka (−3.0%) and cordials (−3.2%).

What comes next?

A few signals point the way.

Producers are already bracing. Grain used in U.S. spirits production dipped 5% in 2024, the first decline after a decade of nearly uninterrupted growth. Because whiskey is distilled years before it’s sold, a pullback in the still house now is a bet that demand stays soft for a while.

Premiumization is narrowing, not ending. The trade-up tide that lifted the whole category for a decade is becoming a story about the top of the market specifically. Expect the gap between the top shelf and everything below it to widen before it closes.

And the squeeze holds until the macro picture eases. As long as essentials stay expensive and confidence stays low, the value and mid-tiers will keep absorbing the most pressure — and brands crowded into the middle will likely lean harder on promotion (temporary price cuts, deals) to hold their ground.

The real headline of 2025 isn’t that Americans drank less, or even spent less. It’s that premiumization didn’t die. It climbed to the top shelf and pulled the ladder up behind it.

Zillah Bahar is the founder of COLAClear, a TTB label pre-screening platform for wine, spirits, and beer.

Source: Distilled Spirits Council of the United States, Annual Economic Briefing, Feb. 5, 2026. Price-tier bands (per 750ml retail): DISCUS/IWSR. Figures are directional.

Related reading: Relationships Won’t Save You. Getting Off the Price Grid Might. — the flip side: how brands escape the price competition premiumization rewards. See also what 13,744 spirits COLAs reveal about how brands actually grow. Getting off the price grid also means getting found: why AI names some wineries and ignores others, on GetDiscoverable.io.